TheWick, Inc. (Wick) has applied for registration as an investment adviser with the U.S. Securities and Exchange Commission. That registration is not yet effective. The information in this article is provided for educational and informational purposes only. It does not constitute personalized investment advice, a solicitation, or an offer of advisory services. No advisory relationship is formed by reading this content.

calendar time isn't the variable that tells you whether an algo strategy is working — trade count and market regime coverage are. three months with 12 trades is not a sample size.

the trade count needed for performance conclusions depends on the strategy — edge size, variance, and trade frequency all matter. for most retail algo strategies, several dozen to a hundred-plus completed round-trips across more than one regime is a reasonable starting point.

operational health and behavioral consistency can be assessed early. performance conclusions can't. the legitimate reasons to stop early are pre-defined risk thresholds and behavior that doesn't match the design — not short-term underperformance.

It's common for retail traders to evaluate an algo strategy by how long it's been running. Three months, six months, a year. That's the wrong variable. What actually tells you whether you have enough data to evaluate a strategy is trade count and market regime coverage — not time.

three months is not a sample size. trade count is. so is regime coverage. you need both before most performance conclusions mean anything.

How many trades do you need before evaluating an algo strategy?

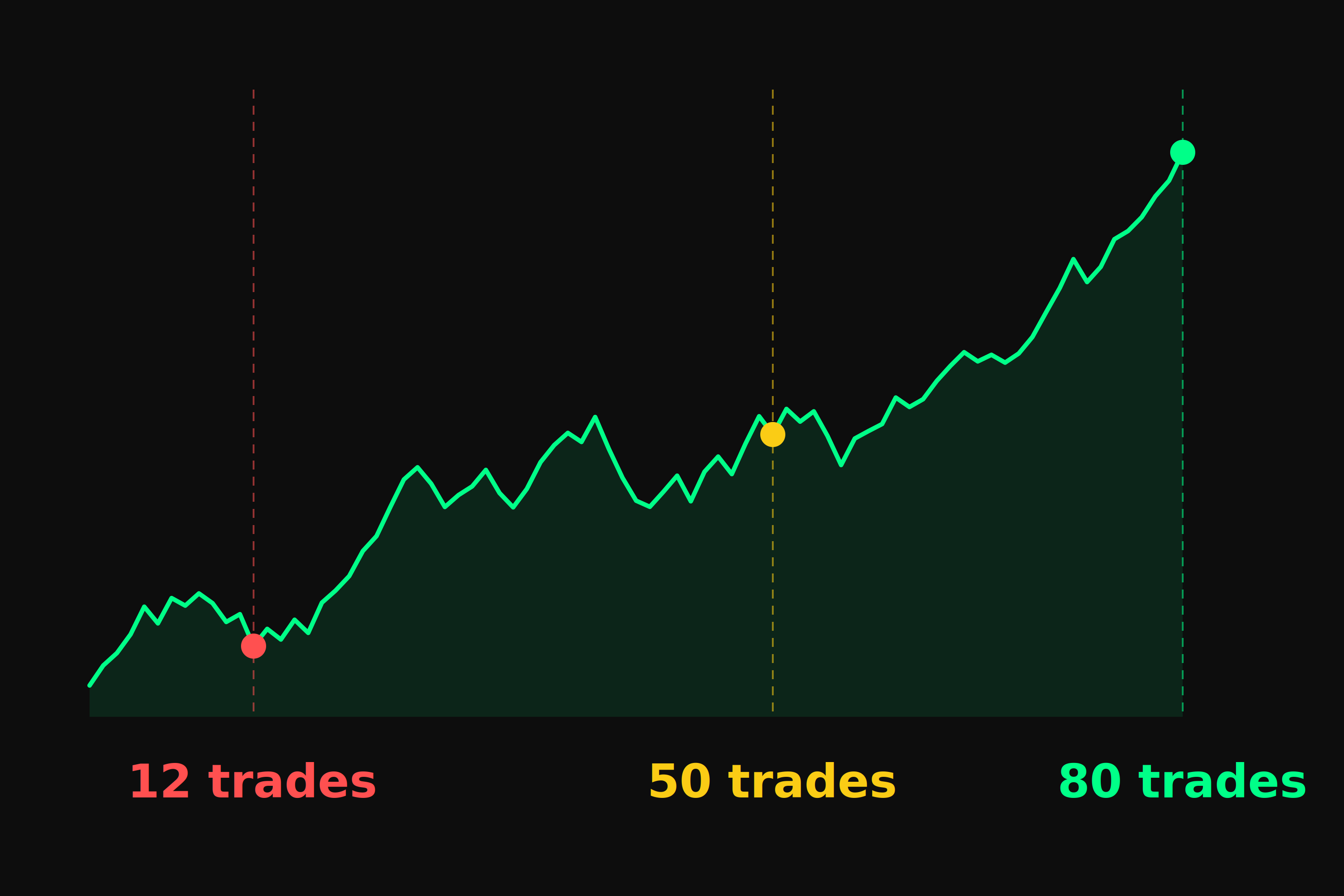

It depends on the strategy. The trade count needed for meaningful performance conclusions is driven by the strategy's edge size, variance, and trade frequency — not by a single universal threshold. For most retail algo strategies, several dozen to a hundred-plus completed round-trips is a reasonable starting point, but the right number is higher for strategies with smaller edges or higher per-trade variance, and lower for strategies with larger, more consistent edges. The closer a strategy's expected per-trade return is to zero relative to its variance, the harder it is to distinguish a real edge from luck — and the more trades you need before a result holds up.

A strategy entering and exiting positions multiple times per day can accumulate a meaningful sample in a matter of weeks. The evaluation question arrives quickly — the sample builds fast.

A strategy trading a few times a month may take many months to a year or more to reach a meaningful sample size. Calendar time understates the data problem — you simply don't have enough trades yet.

It's worth being clear about what "not yet evaluable" means. It doesn't mean the strategy isn't working — it means you don't have enough data to know either way. The strategy is still running, still executing trades, and still generating returns or losses during that window. You're not waiting for something to happen. You're accumulating the sample you need to draw a conclusion from what already is happening.

This cuts both ways. The temptation to exit isn't only when a strategy is losing — it's just as common when it's winning early. A strategy that performs well over 30 or 40 trades can feel like the right moment to take profits and walk away. That's a valid personal decision. What it isn't is evidence that the strategy has confirmed a real edge — an early winning run is no more statistically meaningful than an early losing one. If you exit, exit on your own terms. Just don't mistake a short run of good results for a verdict on the strategy itself.

This matters practically. If you're running a strategy that trades infrequently and evaluating it after three months of losses, you may be looking at 8–15 trades. That's not a conclusion — it's an anecdote. The correct response to a bad run over 12 trades isn't evaluation, it's patience. The exception is if the strategy is behaving in ways that clearly don't match its described logic or historical patterns — that's worth looking at regardless of sample size.

What is regime coverage and why does it matter for evaluation?

Regime coverage describes whether a strategy has been exposed to meaningfully different market conditions — not just accumulated enough trades. A strategy that's only run during a low-volatility trending market hasn't been tested across its operating range, regardless of how many trades it's made.

The regimes that matter most vary by strategy type, but broadly: trending vs. mean-reverting markets, high-volatility vs. low-volatility periods, and risk-on vs. risk-off environments all expose different aspects of a strategy's behavior. A strategy built to capture momentum in trending conditions will look very different during a choppy, mean-reverting market — that's expected. What you're watching for is whether that difference matches what the strategy was designed to do, or whether it's behaving in ways the design doesn't account for.

This is why a strategy with thousands of trades can still have an incomplete picture if it's only run during one market environment. Trade count and regime coverage are both necessary. Neither is sufficient alone.

What can you actually assess before you have enough trades?

Operational health can be assessed almost immediately. Whether a strategy is executing trades consistent with its stated logic, maintaining correct position sizes, and connecting reliably to your brokerage are questions with answers within days, not months.

The distinction between operational health and performance is useful because they have completely different evaluation timelines. Operational problems are worth catching and fixing early regardless of where you are on the trade count curve. Performance conclusions require the sample size and regime coverage described above.

backtests typically model fewer frictions than live execution. live markets introduce slippage, regime shifts, and execution friction that simulations may understate. behavioral consistency is an early indicator, not a verdict. where it earns its keep: catching clear deviations — a strategy trading half as often as described, or losing trades twice the expected size, is worth investigating regardless of where you are on trade count.

When is it actually right to stop a strategy before you have enough data?

The legitimate reasons to stop a strategy before reaching a meaningful sample are fewer than most traders expect. They center on pre-defined risk thresholds and operational failures — not on short-term underperformance.

The honest answer to "how long should I run this before evaluating it" is: long enough to accumulate a meaningful trade count across more than one market regime. For some strategies that's a few months. For others it's a year or more. Calendar time is a starting point for the question, not an answer to it. If you're unsure how a strategy is designed to behave across different conditions, that's worth understanding before you start — not after the first drawdown.