TheWick, Inc. (Wick) has applied for registration as an investment adviser with the U.S. Securities and Exchange Commission. That registration is not yet effective. The information in this article is provided for educational and informational purposes only. It does not constitute personalised investment advice, a solicitation, or an offer of advisory services. No advisory relationship is formed by reading this content.

running multiple algo strategies only diversifies risk if the strategies fail independently. the number of strategies isn't the variable — how independently they draw down is.

strategy type alone is a poor proxy for correlation. two strategies that trade different instruments can share regime dependency and lose in the same conditions. drawdown overlap is the most practically relevant measure.

equal weighting is a defensible starting point when live data is limited. volatility-weighted sizing produces more consistent portfolio behavior once you have enough history to measure each strategy's volatility reliably. allocation deserves periodic review, not one-time decisions.

A common starting instinct when running multiple algo strategies is to split capital equally and move on. Two strategies, 50% each. Three strategies, 33% each. It feels like diversification. It may not be. Running multiple strategies can do two things: reduce risk by spreading exposure across uncorrelated failure modes, or increase edge by accessing multiple independent sources of return. Whether you get either depends almost entirely on one variable — how correlated the strategies are, and specifically how much their losing periods overlap.

Why does correlation determine whether running multiple strategies actually works?

Running multiple strategies can reduce risk or compound edge — but only if the strategies fail independently. A portfolio of five strategies that all draw down simultaneously during choppy, low-momentum markets isn't a diversified portfolio and isn't accessing multiple edges — it's one concentrated bet on market regime, spread across five names. The number of strategies you run doesn't determine what you get. The degree to which they draw down at different times does.

This is why strategy type alone is a poor proxy for correlation. Two momentum strategies — one on equities, one on commodities — can look structurally different but share the same regime dependency. They often struggle together when momentum dies broadly. A momentum strategy and a mean-reversion strategy, by contrast, may be genuinely decorrelated: the conditions that hurt one tend to help the other. What matters isn't what the strategies trade. It's when they lose.

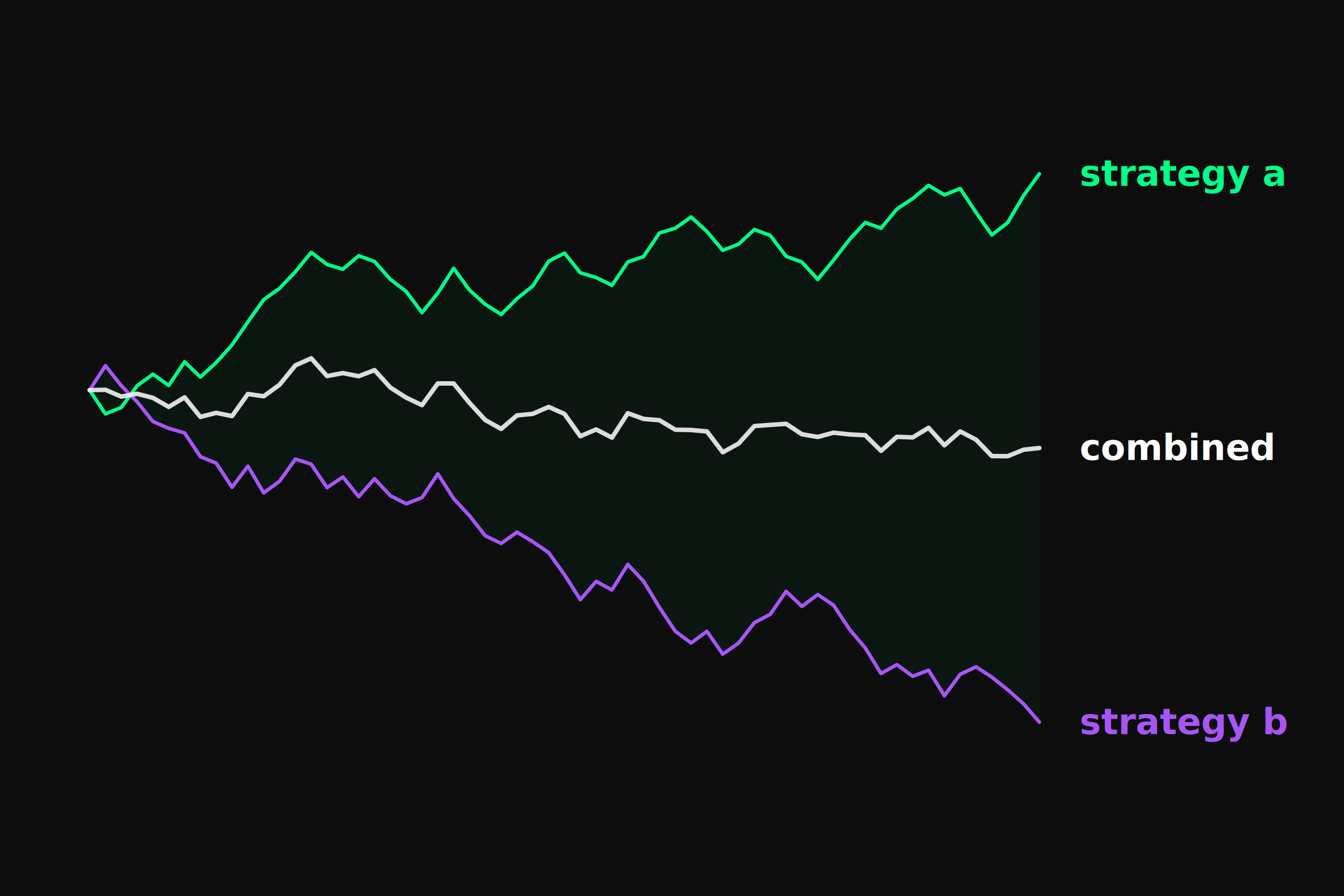

Two trend-following strategies across different asset classes. Same edge, same regime dependency. When trend dies broadly, both draw down. Adding the second doesn't meaningfully reduce risk.

A trend-following strategy and a mean-reversion strategy. The conditions that hurt one tend to benefit the other. Adding the second can genuinely smooth the combined equity curve.

How do you actually measure correlation between algo strategies?

Ideally on live returns, because that's the only data that reflects how both strategies actually behaved in the same market at the same time. If live return history is limited, backtesting both strategies across the same date range gives you a reasonable proxy — the more market regimes that range covers, the more meaningful the correlation estimate.

Before you have enough live data, the most useful proxy is regime sensitivity: what market conditions does each strategy need to work? If both strategies require trending conditions, they are likely correlated regardless of what they trade. If they have opposite regime dependencies, they're likely decorrelated. This is an imperfect heuristic — strategies can share regime sensitivity in non-obvious ways — but it's more informative than looking at instrument or timeframe alone.

Drawdown overlap is the most practically relevant measure. Pull the periods when each strategy has historically drawn down and look for overlap. If they consistently draw down together, adding the second strategy adds correlated risk. If their drawdown periods are largely distinct, you have real diversification.

the question isn't how many strategies you're running. it's how independently they win and lose.

What are the practical approaches to sizing capital across multiple strategies?

Equal weighting is the simplest starting point and often the most defensible when you don't have enough live data to measure correlation reliably. Split capital equally, accept that you don't yet have the data to do better, and let the strategies run until you do. The risk with equal weighting is that a high-volatility strategy at equal dollar weight will dominate portfolio risk even if it represents only a fraction of capital — the volatility, not the allocation, determines its contribution.

Volatility-weighted sizing addresses this by allocating so that each strategy contributes a similar amount of risk to the portfolio rather than a similar amount of capital. A strategy with twice the volatility of another gets proportionally less allocation. This produces more consistent portfolio-level behavior than equal dollar weighting, though it requires enough live return history to measure each strategy's volatility reliably.

Correlation-adjusted sizing goes further — reducing allocation to strategies that add correlated risk and increasing it toward strategies that genuinely diversify. It also requires more data than volatility-weighting alone: enough joint observations across regimes to estimate the correlation reliably, not just each strategy's volatility in isolation. In practice at retail scale, this level of precision is hard to achieve before significant live return history has accumulated. Equal weighting with volatility awareness is usually the right starting point, with adjustments as the live track record develops.

What are the most common capital allocation mistakes when running multiple strategies?

A common mistake is confusing structural diversity for statistical independence. Two strategies that trade different instruments, run on different timeframes, and use different entry logic can still be highly correlated if they share the same underlying edge — particularly regime sensitivity. "They look different" is not evidence they behave differently under stress.

Another is over-diversifying at insufficient capital. Running five strategies at 20% each means each strategy is sized too small to express its edge in any meaningful way after transaction costs, and you don't have enough return history on any of them to measure their correlations reliably. There's a meaningful difference between a portfolio of five well-understood strategies and a portfolio of five strategies that haven't been run long enough to know what they are.

A third is treating allocation as a one-time decision. Correlation between strategies shifts over regime changes. A portfolio that was genuinely diversified in one market environment may become concentrated as regimes evolve. Allocation decisions are often reviewed on a periodic basis alongside individual strategy performance.